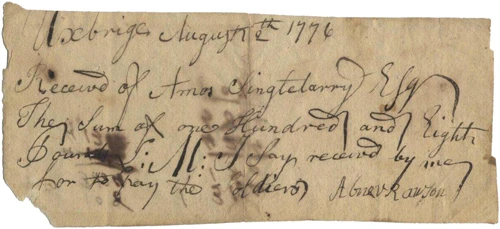

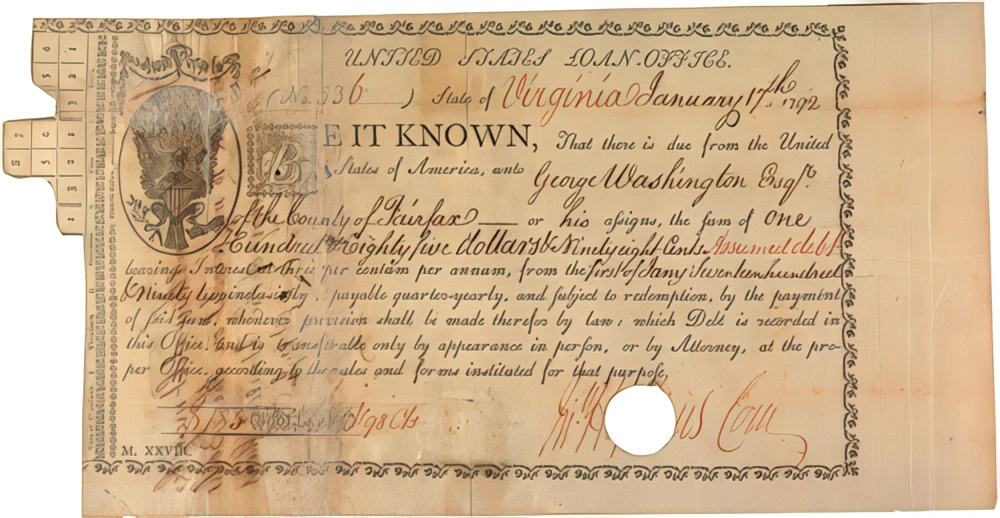

Among the many challenges George Washington faced as the first President of the US, one of the most pressing was the national debt incurred during the Revolutionary War. When Washington took office, the federal government was essentially bankrupt, and its bonds nearly worthless. Federalists like Washington and his first Secretary of the Treasury, Alexander Hamilton, believed the best way to create a lasting republic was to give the central government a vigorous and efficient system of tax collection and public credit. Hamilton, therefore, advocated that the federal government assume, or take over, and then pay the war debts of the individual states.

At Hamilton’s urging, the many federal and state bonds issued during the war were replaced with three types of federal bonds that soon traded at yields around 6%, down from the high double digit yields prevalent just a few years before. In order to pay the interest due on the new bonds, the government established revenues from tariffs, tonnage duties and excises. It also chartered and partially owned a new central bank, the Bank of the United States, which provided loans to the government as well as to merchants and other businesses. Hamilton’s system established the young nation’s credit, and the national debt has existed ever since, with the exception of a brief debt retirement under Andrew Jackson.