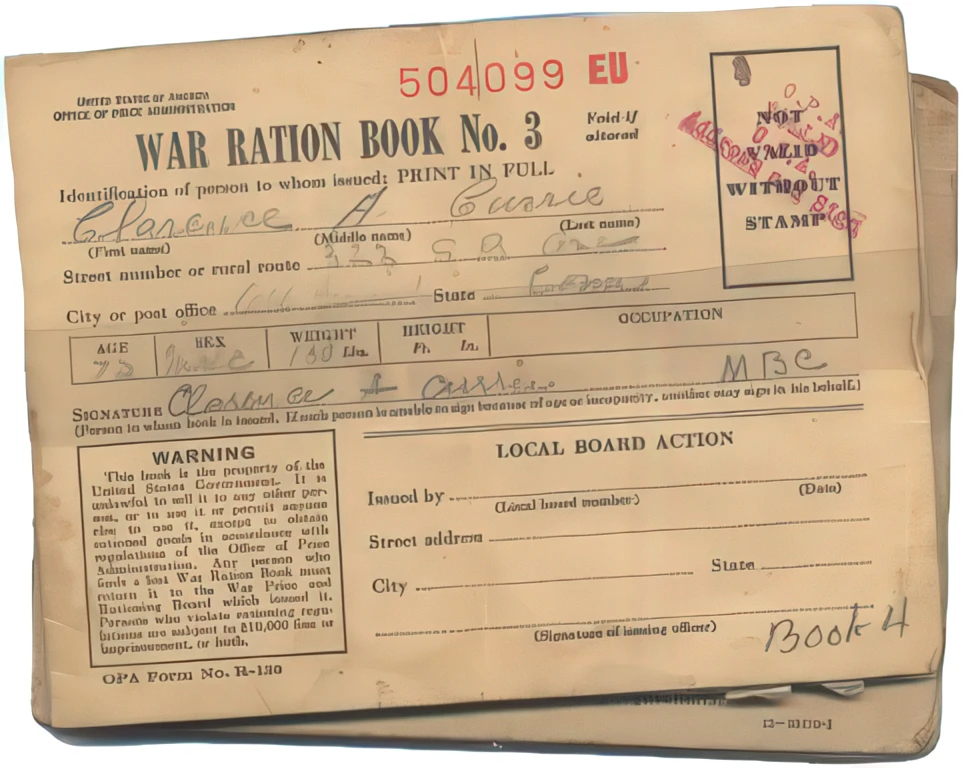

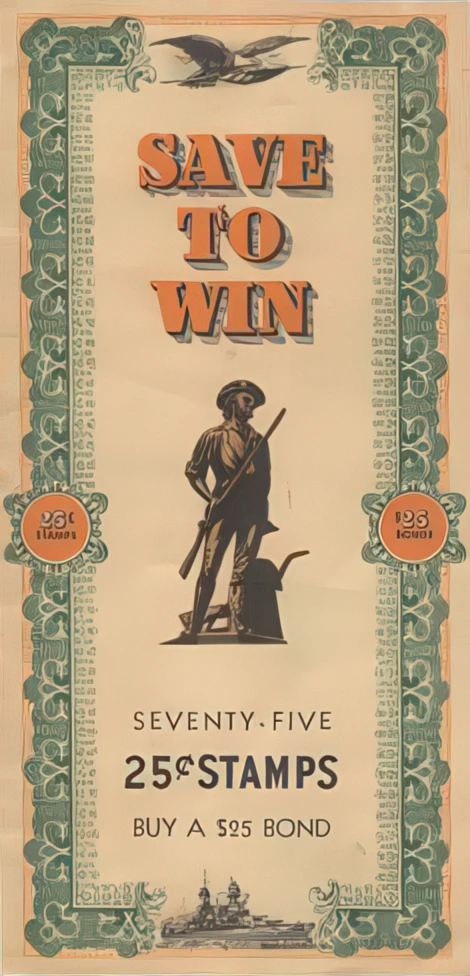

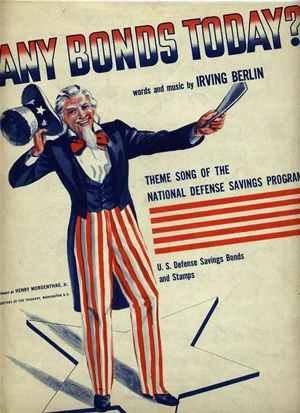

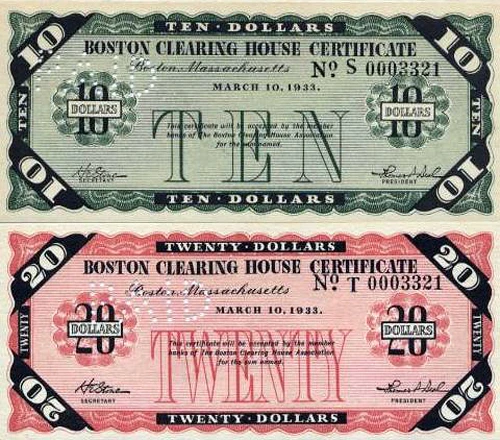

Franklin Delano Roosevelt served longer than any other President, from 1933 to 1945, during a critical period for the country. Inaugurated in the depths of the Great Depression, Roosevelt spent his first two terms trying to fix the broken economy with “New Deal” initiatives. It was his second major financial challenge in office—financing World War II—that eventually returned Americans to work after a decade of double digit unemployment rates. Despite tension between Congress and the President, important financial legislation was passed, and the US successfully funded a war that cost more than all of America’s other wars through the 20th century combined. New Deal legislation was aimed at creating jobs and Social Security, boosting agriculture and industry, supporting unions and regulating banks. By 1940 these policies had given way to revenue and tax bills in preparation for a looming war. Industry revved up production to supply Allied forces and prepare for possible entry into the war, thereby creating jobs and boosting the economy. Like Wilson, Roosevelt and Treasury Secretary Henry Morgenthau believed that taxes should correspond to one’s “ability to pay” and, therefore, favored progressive taxation of businesses and the wealthy. Republicans favored a more broad-based and less graduated system of taxation, such as a sales tax. Tensions ran high in the search for a middle ground, but in the end all Americans were asked to make sacrifices. Income taxes increased significantly over the course of the war, especially for those subject to a special “Victory tax” on larger incomes. Americans were paying for the war with taxes, but were also asked to invest in the war through Victory Bonds, which the government issued in denominations large and small.

Franklin D. Roosevelt

Checks & Balances

Checks & Balances George Washington

George Washington Andrew Jackson

Andrew Jackson Abraham Lincoln

Abraham Lincoln Woodrow Wilson

Woodrow Wilson Franklin D. Roosevelt

Franklin D. Roosevelt

President of the United States (1933-1945)